Examining the Geopolitics of Gas in U.S.-Russia Negotiations

The geopolitics of gas may be shifting again as the United States and Russia revisit LNG sanctions, Nord Stream 2 revival, pipeline transit deals, and potential joint projects.

Over the past decade, the United States has consistently opposed Russian gas exports. Under the first Trump administration, the United States pressured Germany to halt Nord Stream 2, promoted U.S. liquefied natural gas (LNG) globally under the “freedom gas” banner, and pushed Europeans to reduce their reliance on Russia. Following the invasion of Ukraine, the United States banned Russian LNG and later imposed sanctions to stall Arctic LNG development.

But with Trump back in office, the situation has shifted: both U.S. and Russian officials are discussing possible cooperation on gas sales to Europe. Rumors even suggest a revival of Nord Stream 2 or U.S. companies joining Russian upstream and LNG projects in the Arctic. While it’s too early to predict the outcome of the ongoing peace talks, which are driven more by geostrategic motives than market logic, examining the geopolitics of gas reveals several potential scenarios for Russian gas exports to Europe.

Which U.S. Sanctions Are Having the Greatest Impact on Russian Gas Exports?

The United States has imposed numerous sanctions on Russian LNG, targeting equipment, specialized Arctic LNG tankers, and LNG companies like Novatek and projects such as LLC Arctic LNG 2, and starting from January 2025—Portovaya LNG and Vysotsk LNG. These measures have forced all three projects to halt operations, and only Sakhalin-2 and Yamal LNG remain functional.

As for pipeline gas, the United States imposed sanctions related to the Nord Stream 2 and TurkStream pipelines well before the war, in December 2019. On February 23, 2022—just one day before Russia’s invasion of Ukraine—the United States sanctioned Nord Stream 2 AG directly.

What Could Be on the Negotiating Table?

Talks may explore lifting or reinforcing LNG sanctions, easing recent restrictions on Gazprombank, and even reopening Ukrainian transit, which ended on January 1, 2025. Joint U.S.-Russia gas projects have also been floated—an idea as controversial as it is opaque.

It is worth noting that gas sanctions are less critical for the Russian budget than oil or financial sanctions. But symbolically, they matter enormously to Putin. Nord Stream is not just a pipeline—it is a legacy project tied to Putin’s vision of Russia as a dominant energy power in Europe, pursued in defiance of strong opposition from many Western politicians. Its revival would be seen domestically as clear evidence of Russia’s triumph in an existential confrontation with Western liberalism.

Likewise, the LNG projects in Yamal are more than commercial ventures. They symbolize Russia’s global ambitions in a sector where it is a relative newcomer, showcasing its ability to deliver extraordinarily complex Arctic infrastructure—built from scratch, on time, and within budget. More broadly, the projects reflect Russia’s aspiration for dominance in the Arctic and, specifically, control over the Northern Sea Route. Reviving them would signal not only economic re-engagement but also international recognition of Russia’s energy and geopolitical ambitions.

Despite both the United States and Russia, as the leading gas-exporting countries, having an interest in a tight gas market, their commercial interests clash. U.S. LNG players benefit from reduced Russian presence in Europe, so keeping or increasing sanctions would be an acceptable policy for the United States. For Putin, increasing gas exports is important for geopolitical leverage.

Trump’s Options on LNG Sanctions:

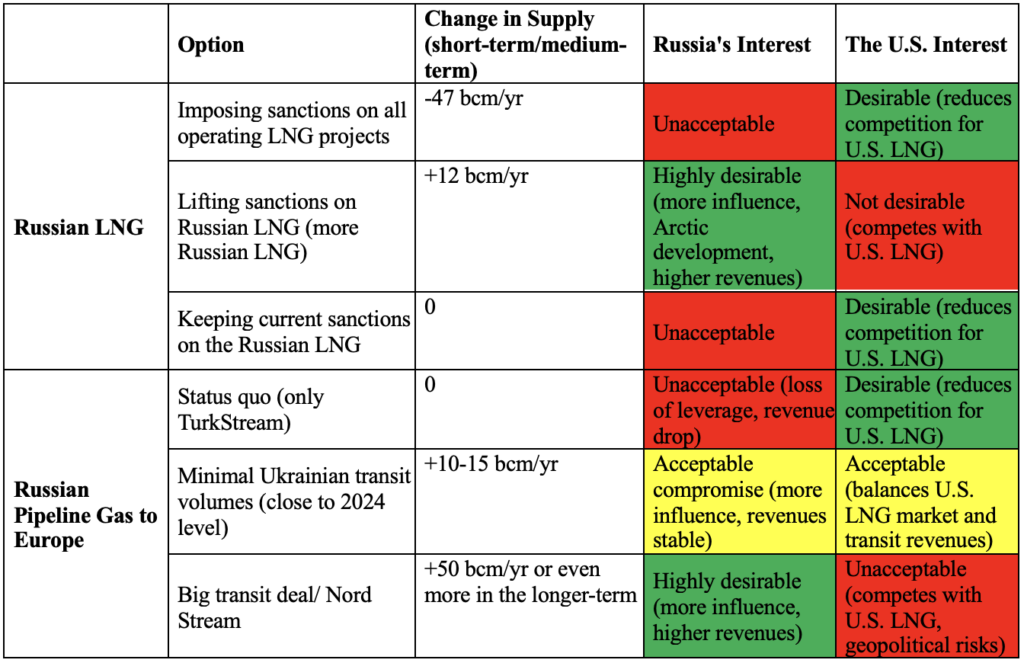

- Strengthen sanctions on Russian LNG. This would be the worst-case scenario for Russia and could quickly remove up to 47 billion cubic meters (bcm) of LNG exports—a boost for U.S. LNG exporters but a move that would infuriate Putin.

- Lift sanctions on Russian LNG (or at least ease enforcement). This would allow more Russian LNG to enter the market, which would hurt U.S. LNG producers, who would face more competition just as the next wave of new LNG capacity and price reductions are expected. The negative impact on U.S. producers could potentially be offset by their participation in Russian LNG projects—though this is unlikely due to political and legal risks—and Chinese shareholders of these projects might object.

- Maintain current sanctions. The status quo preserves the U.S. advantage but won’t satisfy the Kremlin.

Options for Pipeline Gas:

For pipeline gas exports, the situation is even trickier. There are several pipeline routes that could bring Russian gas to Europe, but each has certain constraints:

- The pipeline to Finland will not restart as Finland is preparing to completely ban Russian gas.

- The Yamal-Europe pipeline via Poland is also politically dead.

- TurkStream is already maxed out, and only downside risk remains. It faces growing physical security risks due to attempted Ukrainian drone attacks on supporting infrastructure in Russia’s Krasnodar region. While the attacks have been intercepted, they highlight the pipeline’s vulnerability and exposure to aerial threats and covert operations. Moreover, TurkStream is the only major Russian gas export pipeline to Europe that is still operating at full capacity and thus remains a likely target for additional U.S. sanctions if Washington is dissatisfied with the outcome of negotiations.

- Nord Stream 1 and 2 are damaged and would require a permitting process for repair—aside from one undamaged string, which remains uncertified—not to mention the legal challenges associated with these projects.

- Ukrainian transit ended on January 1, 2025. The last route—via Sudzha—was recently bombed, and the metering station was destroyed. Even if repaired, resumption would take time, as supplies cannot restart immediately.

There are the following realistic options for Russian pipeline gas:

- Status quo. There is no restoration of the pipeline transit deal via Ukraine or Nord Stream, leaving only TurkStream operational. Reduced Russian volumes create more room for U.S. LNG—favorable for Trump but unacceptable for Putin.

- Minimal pipeline transit volumes via Ukraine. Flows return to approximately 2024 levels (10-15 bcm). This could be a mutually acceptable compromise and a potential win-win where Russia preserves some revenue and influence, U.S. LNG remains competitive, Ukraine earns some fees (and may need some of this gas), and countries like Slovakia, Hungary, and others in Central Europe secure a cheap supply.

- Large transit deal/Nord Stream revival. This would take time, as flows cannot restart immediately, but it would eventually bring significantly more Russian pipeline gas into Europe. This would be highly desirable for Russia but politically explosive for Trump unless U.S. companies are able to extract value via transport tolls or upstream shares—an option that remains difficult and legally murky.

Multi-Dimensional Payoff Matrix for Russian Gas Sanctions and Restrictions

Strategic Crossroads

Trump faces a three-way balancing act: keeping energy cheap at home, expanding U.S. LNG abroad, and developing a symbolic peace deal. However, he wants fast, high-visibility wins over complex resolutions. Meanwhile, Russia is trying to shift the discussion away from the Ukraine conflict and toward broader U.S.-Russia economic cooperation—floating joint projects on rare earths, Arctic cooperation, and gas. Will this tactic work? That remains to be seen. But any shift in gas sanctions will have a ripple effect across global gas markets. Russian volumes are a real wildcard: whether they return or disappear, they will impact prices, gas flows, financial investment decisions on new projects, and the geopolitics of gas.

Tatiana Mitrova is a Research Fellow at Columbia University’s Center on Global Energy Policy and Director of the New Energy Advancement Hub.

Image: Fly of Swallow Studio/Shutterstock